Pre-Election Jitters

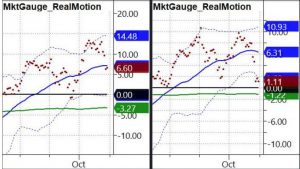

Equity Indexes retesting the September Low amid growing volatility just ahead of a potentially contentious presidential election next week. 89% of stocks traded below their 10 DMA average on Friday. The market is still looking for another major round of stimulus/relief, but that has been delayed until at least after the election. Small and mid-caps have been holding up the best amid the recent sell-off with a slight shift from growth into value stocks. KRE was the lone member of the Economic Modern Family to buck the down move on Friday.

Equity Indexes retesting the September Low amid growing volatility just ahead of a potentially contentious presidential election next week. 89% of stocks traded below their 10 DMA average on Friday. The market is still looking for another major round of stimulus/relief, but that has been delayed until at least after the election. Small and mid-caps have been holding up the best amid the recent sell-off with a slight shift from growth into value stocks. KRE was the lone member of the Economic Modern Family to buck the down move on Friday.

The highlights of this week’s market action are the following:

- Risk gauges are negative

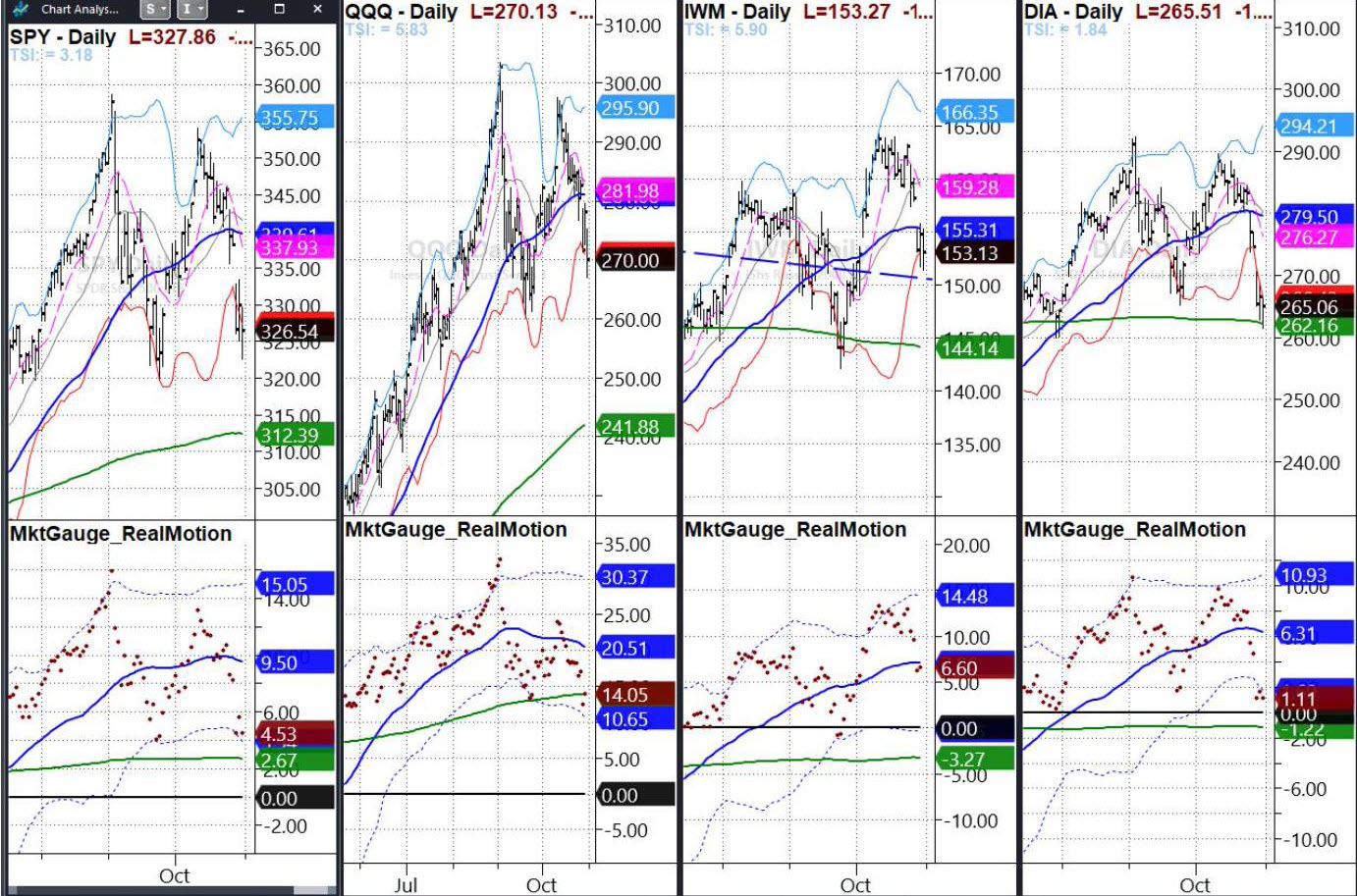

- DOW oversold – running weak – could bounce off 200 DMA

- Volume patterns show hardly any accumulation days as markets sold off. Markets still in distribution condition.

- Risk-off safety play like Utilities down less than overall market

- Long volatility (risk-off play) up almost 20 percent

- Oil & Gas leading down movement – down -10% on average – Oil and Gas Exploration hit worst

- McClellan oversold – but not at extreme levels from March 2020

- Next critical area in the SPY under 320 and 312

- 89% of Stocks under 10 DMA

- US Bonds (TLT) failed at 200 DMA – major issues with potential top and head and shoulders pattern continuing to play out.

- Small and Mid-caps are holding up better than big and mega cap stocks.

- Value and Growth both look bad

- KRE (Regional Banks) closed up on Friday – 5 of 6 Economic Modern Family sectors dropped – KRE has been weak but strong counter-move this week

- From the mid-May low in the EEM/SPY ratio, EEM up approximately 20% vs SPY up around 10%.

Stay One Step Ahead of The Markets and Profit

From The Current Volatility With Market Outlook